Iran, Hormuz, and The New Industrial Tax

What looks like geopolitics on television is already showing up in freight rates, insurance, fuel, lead times, and executive decision-making.

A week or two ago, this conflict was still mostly a geopolitical story.

It has since turned into something else entirely.

Clearly, it’s about energy. But it is also about shipping, about air freight, about insurance, about plastics, about timing, and, increasingly, about management. What looks like war on television is already entering the physical economy as a kind of tax - not a formal tax, of course, but a tax all the same: on movement, on certainty, on margin, and on time.

That is what this first issue of Shockwatch is about.

We are not going to predict where missiles land next, nor tell our readers who is morally right, nor compete with war correspondents. There are already enough people doing those things. Our take is much narrower and, we think, more useful for busy operators: when a conflict starts pushing on chokepoints, prices, routes, insurance, and industrial inputs, what does that actually mean for the people trying to source, design, price, ship, and plan? That is the question.

And as of Friday, 13 March 2026, it is no longer a theoretical one. (IEA)

From war to throughput

A useful mistake to avoid is to think of the Strait of Hormuz as a dramatic geography lesson, while it isn’t. It is a story on infrastructure. The kind of infrastructure that we have long taken for granted, because it usually just works.

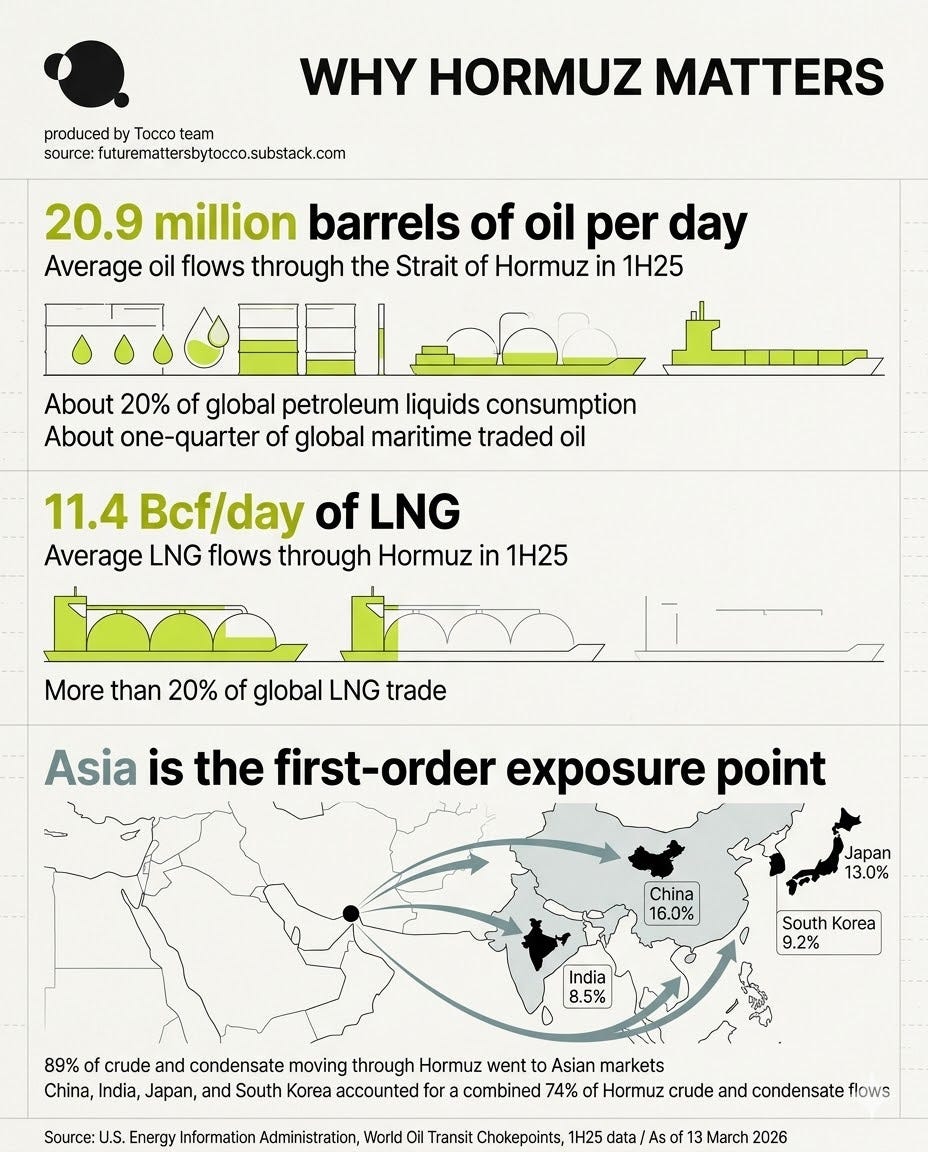

According to the U.S. Energy Information Administration, around 20.9 million barrels of oil, per day, moved through Hormuz in the first half of 2025, equal to roughly 20% of global petroleum liquids consumption. On top of that, about 11.4 billion cubic feet per day of LNG transited the strait, which was more than 20% of global LNG trade. The same analysis says 89% of the crude oil and condensate moving through Hormuz went to Asian markets, with China, India, Japan, and South Korea accounting for 74% of those flows. This is why the strait matters so much: not because it is famous, but because the physical economy is still routed through a very small number of critical passages. (IEA)

That kind of concentration is easy to forget in calmer periods. The world economy often gets described as a giant web, while in reality, it is much less web-like, being closer to a relay race with a surprisingly small number of critical handoff points. And when one of those handoff points becomes unreliable, the damage does not stay politely at the chokepoint. It spreads like wildfire.

Already historic

The International Energy Agency said on 11 March 2026 that its 32 member countries had agreed to make 400 million barrels of oil from emergency reserves available to the market, describing the move as the largest collective stock release in the agency’s history. The IEA also said oil flows through Hormuz had been so badly disrupted that exports of crude and refined products were running at less than 10% of pre-conflict levels. (IEA)

A day later, Reuters reported that the IEA now sees the conflict as the largest oil supply disruption in the history of oil markets, with global oil supply in March expected to fall by 8 million barrels per day. Reuters also reported that Brent, which had spiked earlier in the week to $119.50, was still hovering near $97 on 12 March. (Reuters)

Those are not normal numbers. While they do not mean the world is ending, they do mean this situation is no longer something that can be filed away mentally under “news to skim later”. A record reserve release is the kind of signal that tells you the market has already moved past anxiety into intervention. (IEA)

The Re-pricing of Movement

The easiest version of the story is: war in the Middle East, increasing oil prices.

This is true, no doubt. But it’s also grossly insufficient.

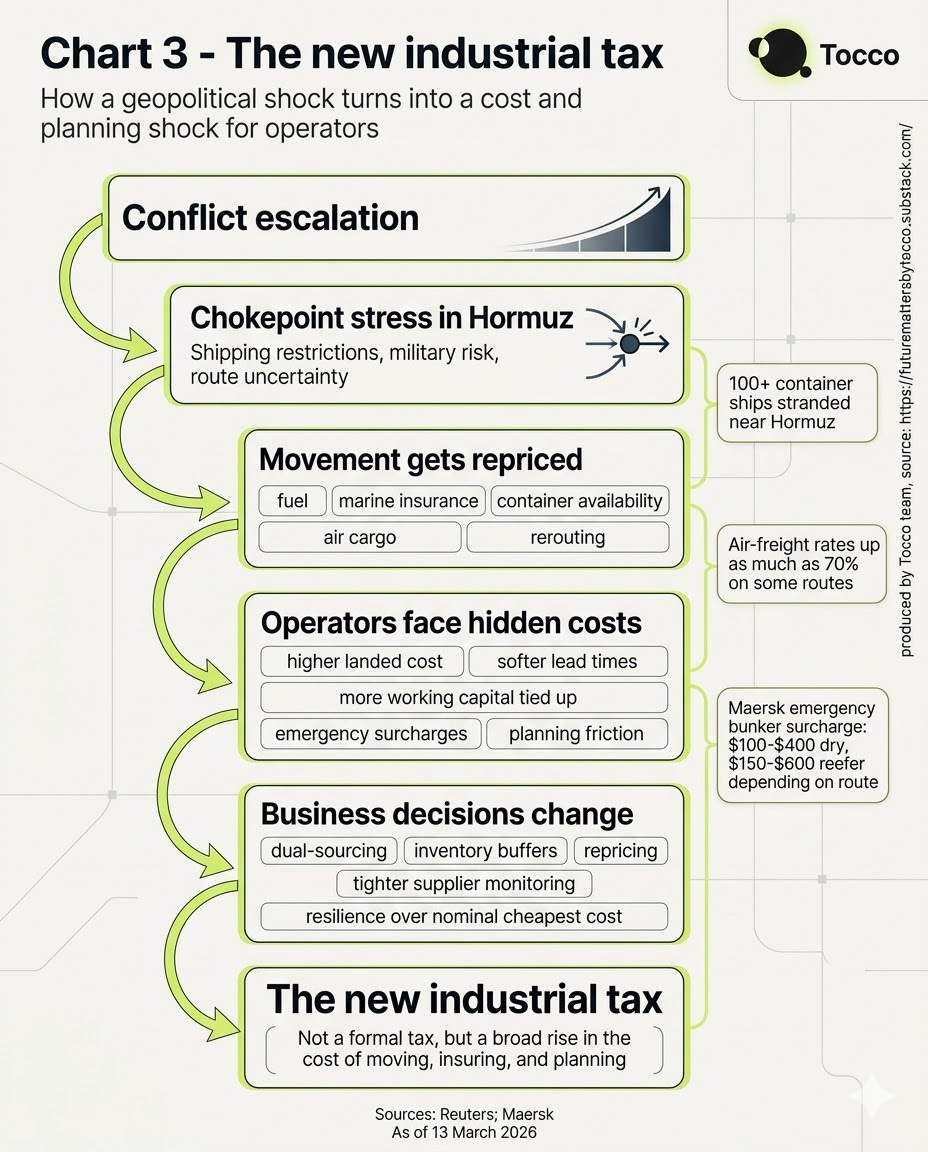

By diving deeper, you’ll see that once a strategic corridor becomes militarily risky, the cost of moving things through the system starts being repriced, all at once. That repricing shows itself through several channels:

fuel

marine insurance

tanker and container availability

route reliability

air cargo spillover

inventory and working-capital stress

Reuters reported today that air-freight rates have risen by as much as 70% on some routes, driven by a mix of airspace closures, ocean shipping blockages, and much higher jet-fuel costs. In the same report, they also said more than 100 container ships have been stranded near Hormuz. It also pointed to disruptions on South Asia-Europe lanes and pressure on hub airports in the Gulf, such as Dubai and Doha, with a butterfly effect for cargo moving far beyond the Gulf itself. (Reuters)

This is the part many executives miss at first. They assume the impact is localized, which cannot be further from reality for impacts of this scale. If sea lanes are delayed or restricted, some cargo shifts to air. If airspace is disrupted, air capacity tightens and prices jump. If insurance and war-risk premiums rise, schedules become less trustworthy even before routes formally close. The result is that a geopolitical event very quickly snowballs into a systematic event.

And it’s in systematic events that costs start hiding in plain sight.

Maritime Risk is Real

Reuters reported on 12 March that Iran said ships must coordinate with its navy when passing through the Strait of Hormuz. Reuters also published a tracker the same day saying 16 civilian ships had been attacked since the beginning of the conflict, citing data from the Institute for the Study of War and AEI’s Critical Threats Project. (Reuters)

It’s one thing to worry about physical danger, but for logistics networks, perception holds as much water as reality. Once shipowners, insurers, freight forwarders, and cargo owners begin treating a route as unpredictable, the route is effectively damaged even before it is fully closed. Capacity becomes harder to secure. Surcharges appear. Alternatives become crowded. Lead times become softer. Contracts that looked acceptable under normal assumptions start looking thin.

This is why we think the best frame for what is happening is not “oil shock” alone. It is an industrial risk premium. The physical economy is being asked to pay more, and plan harder, for the same act of moving goods through the system. (Reuters)

Asia is first. Europe is next.

The EIA data makes the first part very clear: Asia is more directly exposed because most crude and condensate moving through Hormuz heads there, and China is the largest LNG destination among countries supplied through the strait. (IEA)

That should not lead European teams to relax. Europe does not need to be the first-order buyer to feel the consequences. It only needs to live in the same market for:

energy

freight

synthetic feedstocks

petrochemicals

plastics

insurance

industrial sentiment

That is the point. In a fragmented but still connected world economy, disruptions do not need to touch you directly to become your problem. They can arrive through benchmark prices, rerouted cargo, constrained capacity, nervous suppliers, and cautious customers. The more energy-intensive, time-sensitive, or shipping-dependent your operations are, the more quickly the shock becomes visible. (IEA)

An Uneven Tax

This is where the story becomes more managerial than geopolitical.

The firms most exposed are not necessarily those with the highest headline energy bill, but very often the firms that are brittle in less obvious ways:

firms with long or fragile lead times

firms over-reliant on one sourcing region

firms dependent on petrochemical-linked inputs

firms that still model landed cost using last quarter’s freight assumptions

firms with poor visibility into second-order supplier exposure

Those second-order effects matter because the market rarely punishes everyone equally. It punishes the unprepared first. One company will absorb higher shipping or air costs and move on. Another will miss a delivery window, switch transport mode at the worst possible moment, and discover too late that the “cheapest” supplier on paper came with no resilience built in.

This is why the new industrial tax is not just about crude prices. It is about the cost of uncertainty entering systems that were optimised for smoothness rather than stress. (Reuters)

Questions for Serious Operators

The right response is not panic, but discipline.

A few questions are worth asking this week:

Where do we have direct or indirect exposure to Gulf-linked energy, LNG, petrochemicals, plastics, or shipping lanes?

Which suppliers become fragile if ocean transit remains disrupted for another two to six weeks?

Which landed-cost assumptions are now stale?

Where would we be forced into air freight, and what would that do to margin?

Which categories deserve dual-sourcing, tighter monitoring, or more inventory buffer than they had a month ago?

These are not dramatic questions. That is precisely why they matter. In times like this, the operational edge usually comes from asking the unglamorous questions faster than everyone else.

What we are watching next

There are four things we would watch from here.

First, whether commercial movement through Hormuz meaningfully normalises, or remains technically open but commercially impaired. The difference matters.

Second, whether air-freight rates continue climbing or start to stabilise. Reuters did note early signs that rates may be levelling as carriers add capacity and some Gulf operations resume. (Reuters)

Third, whether the shock spreads more visibly into chemicals, plastics, and manufacturing feedstocks, that would broaden the story from energy and logistics into direct material-cost pressure.

Fourth, whether executive behaviour changes. Because these moments tend to accelerate trends that were already underway: dual-sourcing, regionalisation, more appetite for redundancy, and a greater willingness to pay for visibility rather than simply chasing the lowest cost.

That may be the longer-term consequence of this episode. Not the end of globalisation, not the end of trade, not some lazy “deglobalisation” cliché. Something more practical than that: a world in which resilience keeps getting repriced upwards, one shock at a time.

And that is why this should not be filed as “just another foreign-policy crisis”.

It is already a business story.

It is already a systems story.

And for more teams than they realise, it is already a cost story.

- By Leon Ge, on behalf of the Tocco team

Friday 13 March 2026

Private invitation: FutureMade China

A small group of founders, investors, and senior operators will join us in 2026 for a closed-door immersion into China’s industrial frontier - from advanced manufacturing and robotics to AI, biomanufacturing, and the ecosystems shaping the next decade. If you want to see the China that most executives never get access to, apply for an invitation here.