Germany built the old automotive playbook. China is now reviving it.

What if the most important story in cars today is not that China is “winning” and Germany is “losing”?

What if the deeper story is that China has revived, at a much harsher clock speed, some of the very industrial instincts that once made Germany formidable in the first place?

That is the frame I would offer.

After two decades living and working between China, Singapore, France and wider Europe, and after spending the last few years visiting Chinese industrial hubs, industrial parks, suppliers, founders, manufacturers, and local officials across the country, I have come to think that the car story is widely described but still badly understood.

Too many people still tell it as a simple EV story.

It is not.

It is an operating system story.

And Germany, for all its prestige, is now being forced to compete against a newer and harsher one.

Germany’s old formula was real

For a very long time, Germany’s automotive strength rested on a formula that was powerful enough to feel almost natural: engineering prestige, supplier depth, export discipline, industrial consensus, relatively cheap energy, and a highly profitable relationship with China. Reuters put it more bluntly in 2024: Germany’s long-time formula relied on cheap energy from Russia, lucrative trade ties with China, and consensual industrial relations. That formula is now under strain on all three fronts. (Reuters)

This is why the current pressure on German carmakers should not be read as a normal cyclical wobble.

It is not one bad quarter.

It is not merely that EV adoption is difficult.

It is that the environment that once made German automotive excellence scalable has become less forgiving, while the environment that now favours speed, software, battery economics, and brutal iteration increasingly points elsewhere. (Reuters)

The scoreboard is ugly enough already

The recent numbers are not subtle.

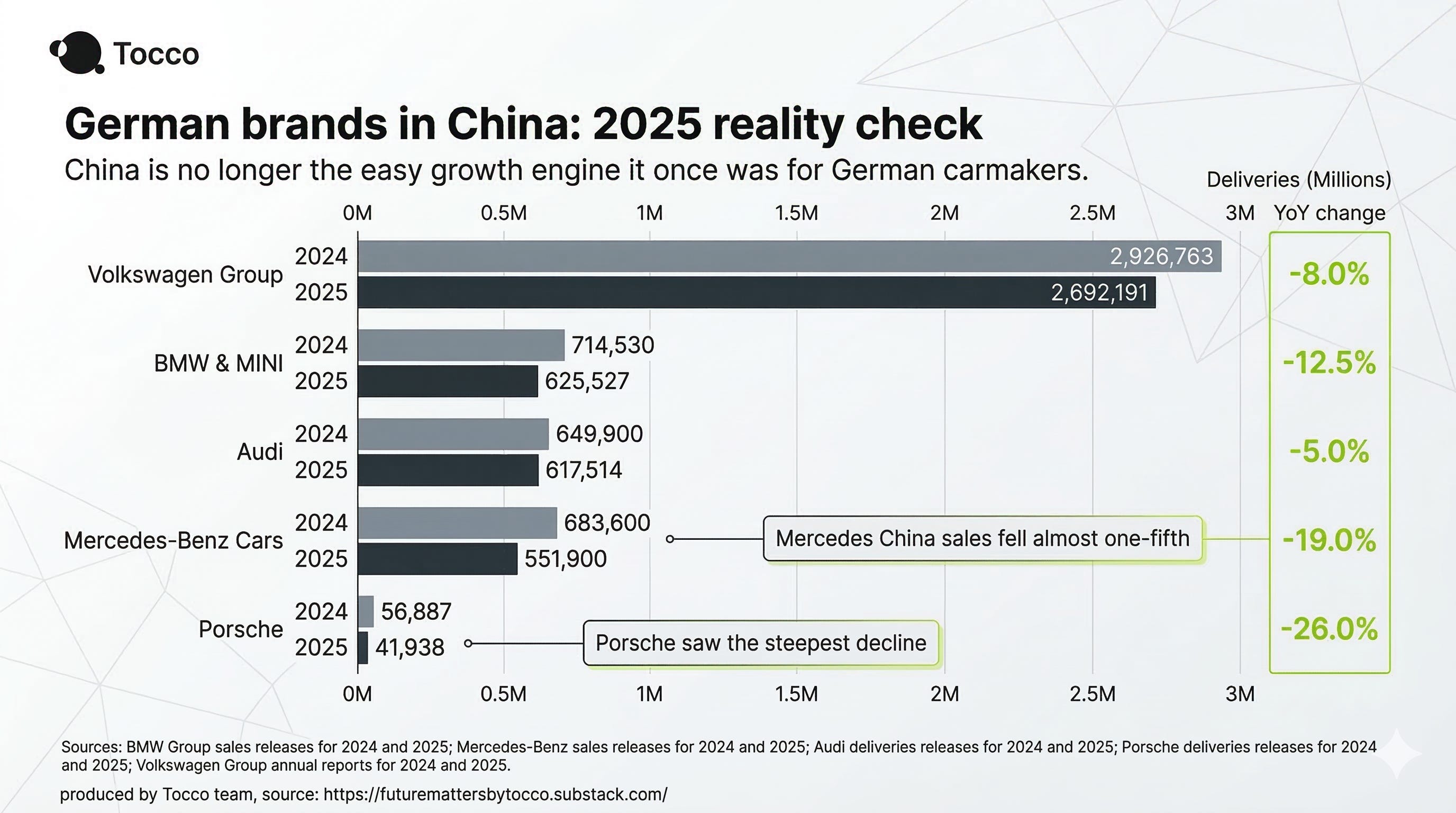

Mercedes-Benz Cars sold 1.80 million vehicles in 2025, down 9% year on year, with China down 19% to 551,900 units. BMW Group’s sales in China fell 12.5% to 625,527 vehicles. Audi delivered 617,514 vehicles in China, down 5%. Porsche’s China deliveries fell 26% to 41,938 cars, while group operating profit collapsed from €5.64 billion to €413 million and its operating return on sales fell to 1.1%. Volkswagen Group’s total deliveries were broadly stable at 8.98 million vehicles in 2025, but China deliveries fell 8%, and its battery-electric deliveries in China fell 44.3% to 115,500 units. (Mercedes-Benz Group)

None of this means German carmaking is dead. That would be lazy.

Volkswagen has just reclaimed the top-selling position in China in the first two months of 2026 with a 13.9% market share, narrowly ahead of Geely at 13.8%, while BYD fell to 7.1% after subsidy changes and fading tax incentives hit the market. Audi has regained the leading premium position in China. BMW remains globally large and profitable. Mercedes still dominates the over-1-million-RMB segment in China. Porsche’s 911 continues to be an icon. (Reuters)

But that is precisely the point.

This is not an obituary.

It is a stress test.

The deeper problem is not “EVs”. It is tempo.

If you reduce the story to “German carmakers were slow on EVs”, you miss the real shift.

The real shift is tempo.

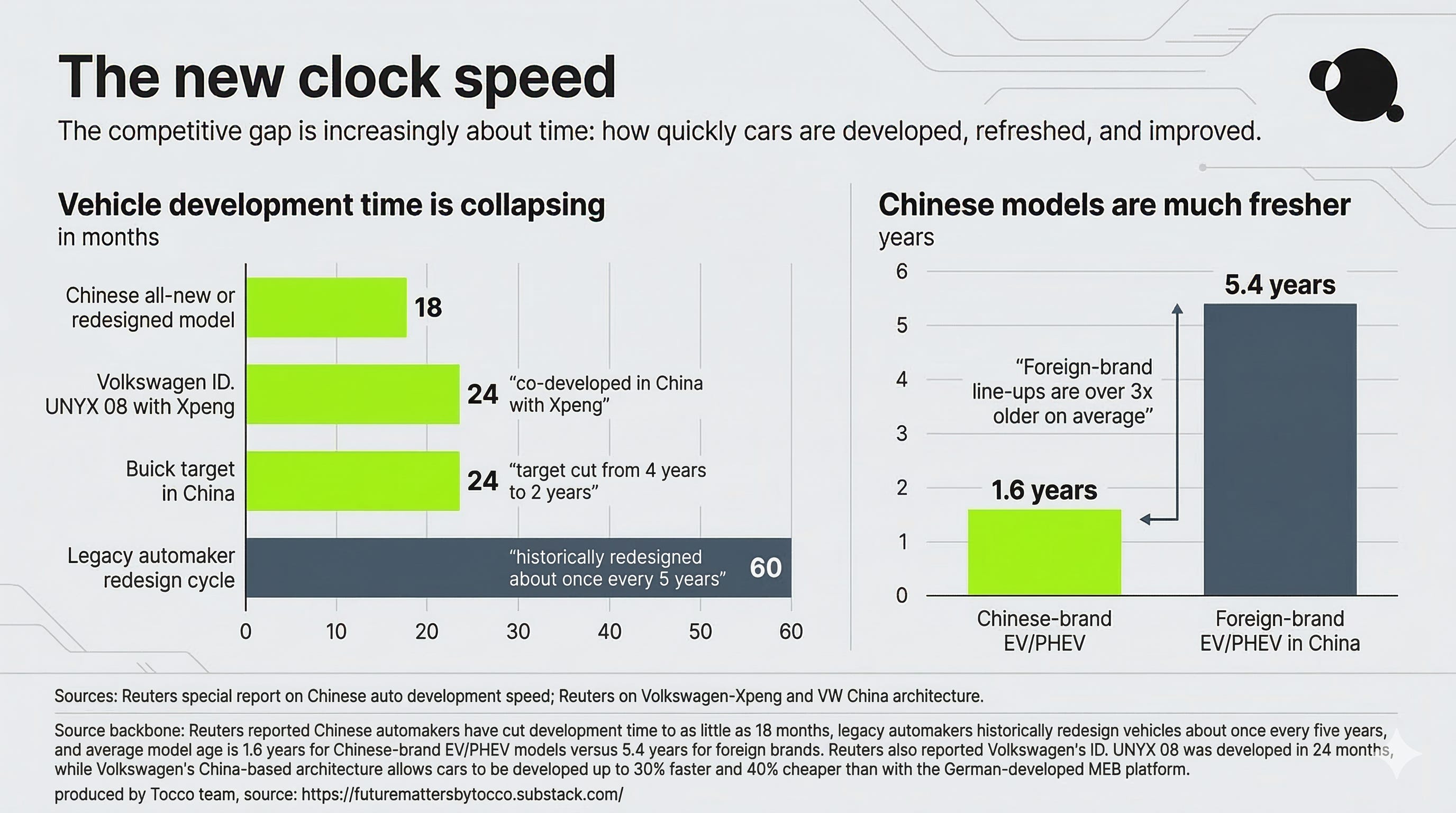

Chinese automakers and suppliers do not merely produce electric cars. They compress time. They compress model cycles, software updates, supplier response times, localisation speed, charging infrastructure deployment, and the willingness to ship before every last uncertainty has been philosophically resolved.

Volkswagen’s own response tells the story. It’s the first mass-produced EV developed with Xpeng, the ID. UNYX 08 reached production in 24 months. Reuters reports Volkswagen says its new China-based architecture allows vehicles to be developed 30% faster. The group plans more than 20 new models in China in 2026 and 50 new-energy vehicles there by 2030. That is not the behaviour of a company making cosmetic adjustments. That is the behaviour of a company being forced to adopt a new clock. (Reuters)

That is why I do not think the best frame is “China has overtaken Germany”.

The better frame is this:

Germany still carries much of the brand equity of the old automotive order.

China increasingly carries more of the operating logic of the new one.

And the wider German system is under pressure too

Cars do not exist outside industrial conditions.

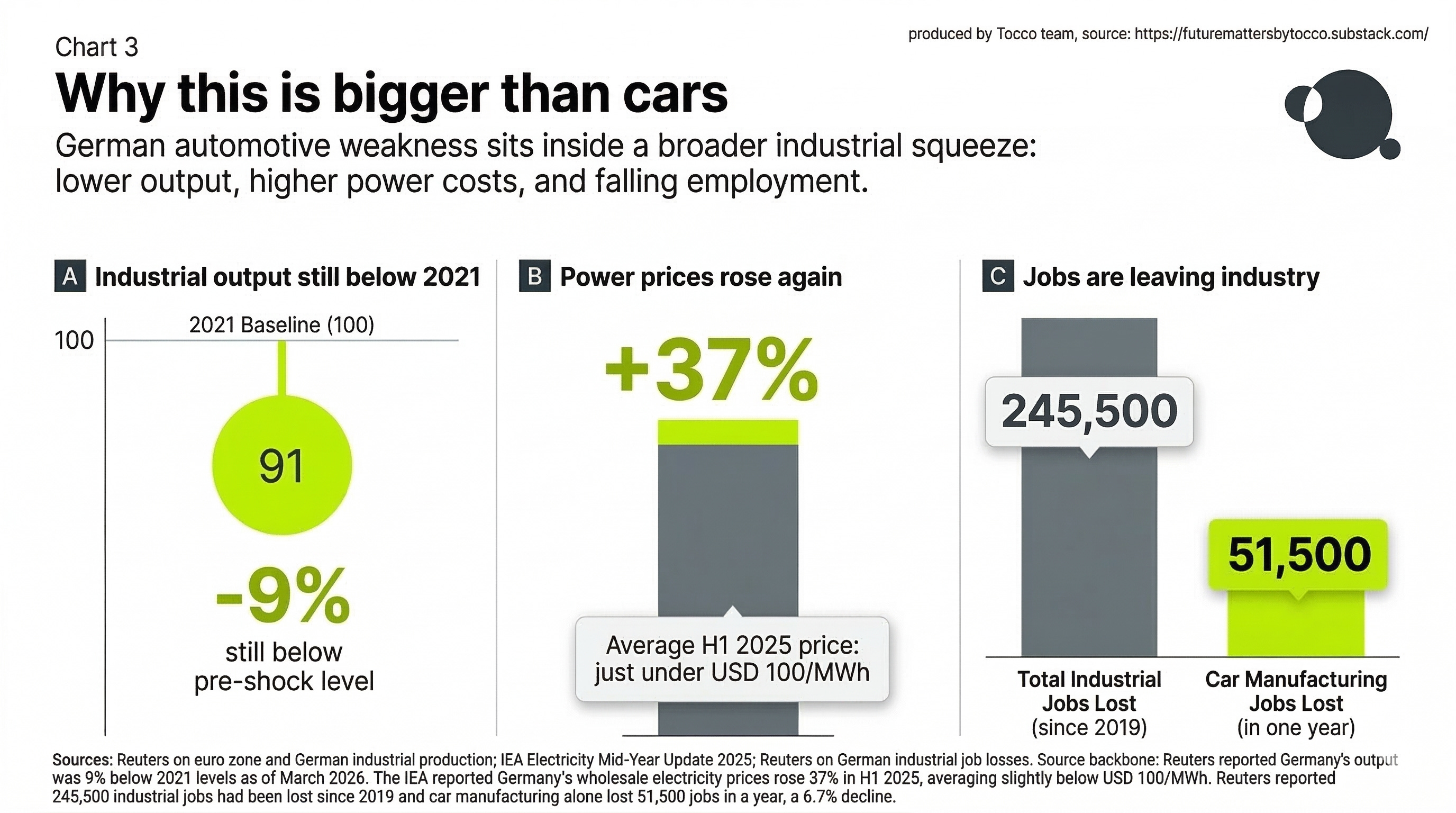

German industry is not being tested only by BYD, Geely or Xiaomi. It is being tested by energy, labour costs, slower growth, tariff pressure, and a broader erosion of the old business environment. Reuters reported last week that euro zone industrial output is now 3% below its 2021 level, and Germany has been one of the hardest-hit countries, with output 9% below 2021 levels. The same report points to high energy costs, competition from China, U.S. tariffs, poor productivity growth, and weak global demand for European cars as the reasons. (Reuters)

The energy side matters more than many people want to admit. Reuters noted in February that Germany had for decades relied on relatively cheap Russian gas, which had been a key industrial advantage. The IEA also reported that German wholesale electricity prices rose 37% in the first half of 2025, with average prices just below USD 100/MWh. In other words, Germany is trying to run a manufacturing-heavy model after losing one of the inputs that helped make that model work. (Reuters)

The labour side is becoming visible too. Reuters reported in August that German industry had shed around 245,500 jobs since 2019, and that the sharpest annual decline was in car manufacturing, where around 51,500 jobs were lost in a year. Volkswagen alone is planning major cuts through 2030. (Reuters)

China’s automotive machine is bigger than most people still realise

China is not only making more EVs. It is becoming the centre of gravity for the industrial learning curve itself.

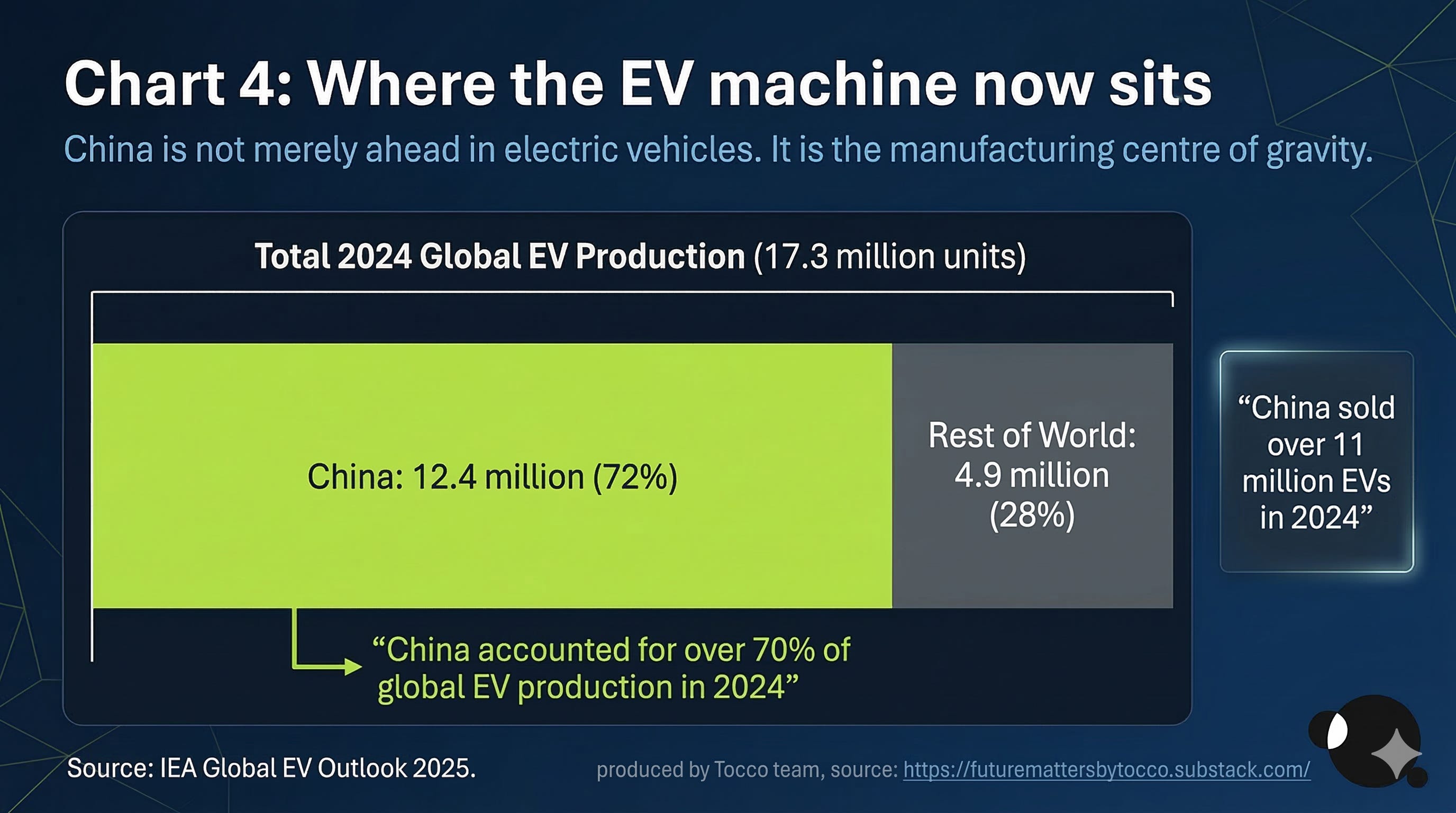

According to the IEA, China produced 12.4 million electric cars in 2024, more than 70% of global EV production. China also sold over 11 million electric cars in 2024, with electric vehicles accounting for almost half of all car sales in the country. That is not just scale. That is training data for an industrial system. (IEA)

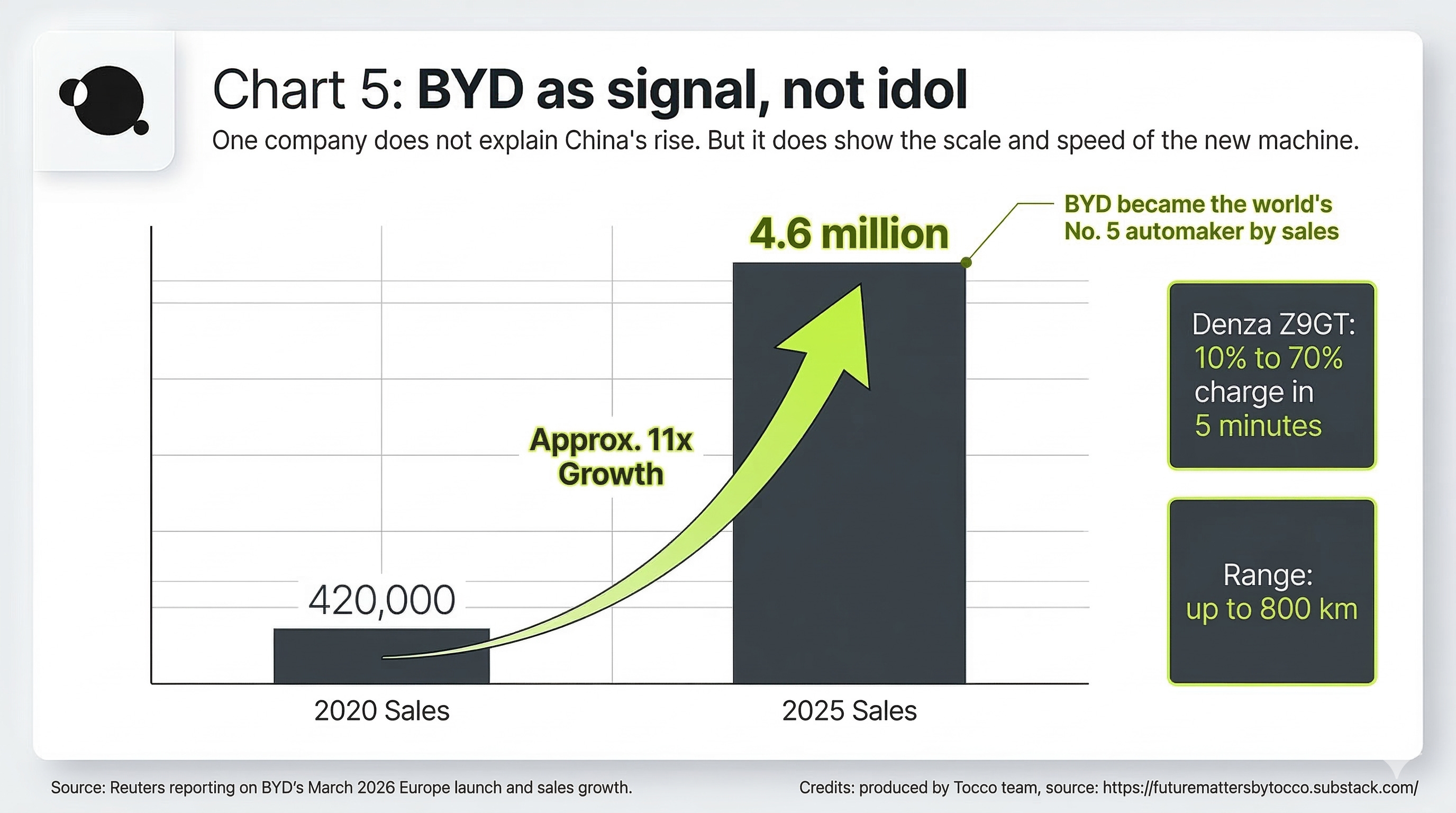

And the speed frontier keeps moving. Reuters reported last week that BYD’s Denza Z9GT will launch in Europe with charging from 10% to 70% in five minutes, with up to 800 km of range, while BYD’s own sales grew from 420,000 cars in 2020 to 4.6 million in 2025. Even if specific models or subsidy conditions fluctuate, the direction of travel is unmistakable. (Reuters)

But here is the nuance most lazy articles miss

China’s automotive rise is not clean.

It is not smooth.

And it is not built on pure profitability or Western-style market hygiene.

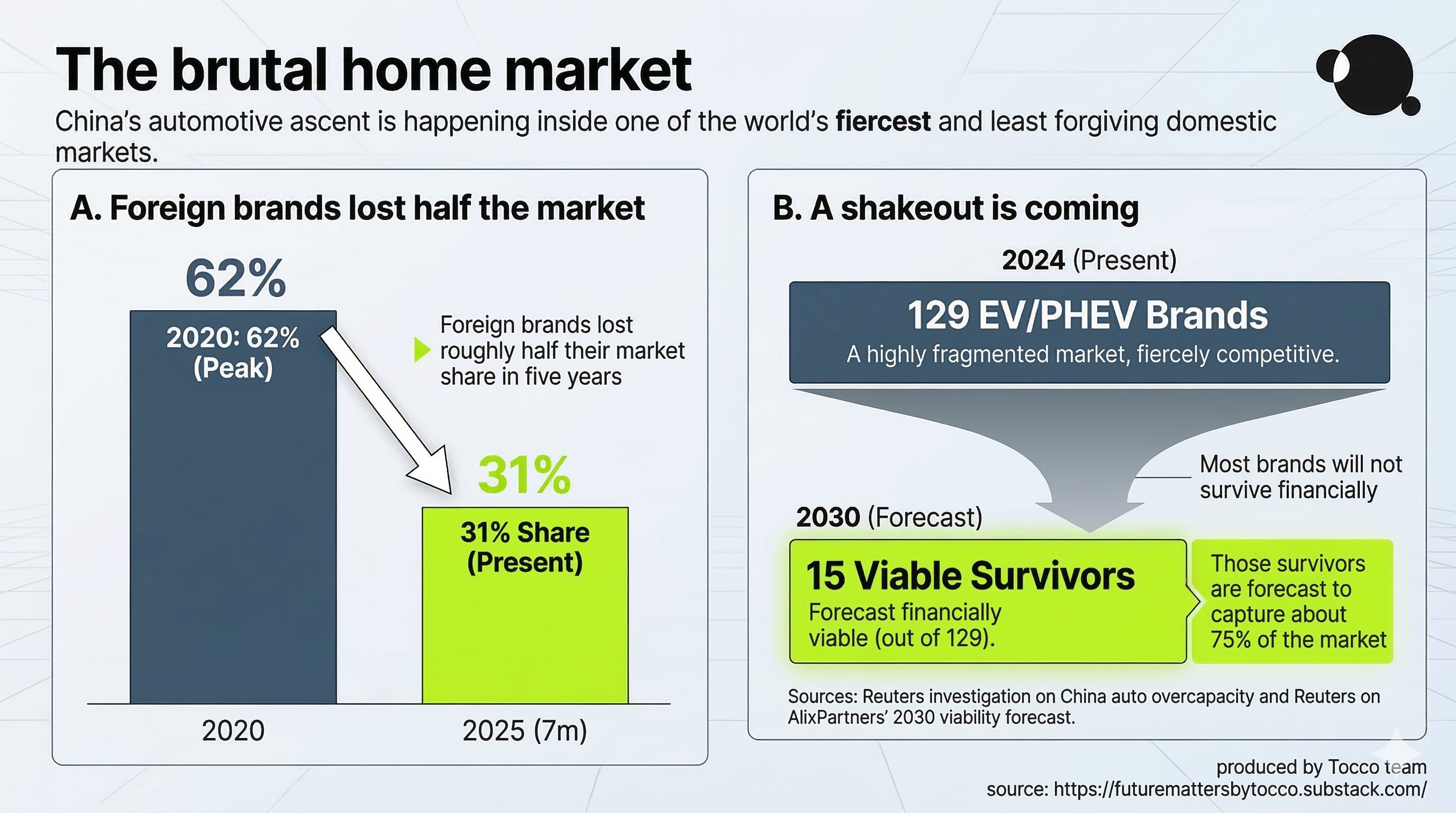

Reuters reported in September that foreign brands’ share of China’s car market fell from 62% in 2020 to 31% in the first seven months of 2025. But the same Reuters investigation also found an oversupplied market, deep discounting, local-government inducements, pressure to keep factories running, and a system in which capacity has outrun rational demand. AlixPartners estimates only 15 of China’s 129 EV and hybrid brands may be financially viable by 2030. (Reuters)

This matters because it sharpens the argument.

China is not winning because everything is tidy.

China is winning, in many layers of the value chain, because the system is willing to be harsher, more compressed, more subsidised, more localised, and more brutally competitive than most incumbents in Europe or Japan would comfortably tolerate.

That has obvious risks.

It also creates speed.

This is why “premium” no longer means what it used to mean

For years, German premium brands benefited from a simple asymmetry.

China made many things.

Germany made the aspirational car.

That asymmetry is weaker now.

The new Chinese rivals are not just cheaper. They are increasingly software-rich, fast-moving, and in some segments more aligned with what younger buyers want: digital interfaces, rapid refresh cycles, ambitious charging, strong in-cabin experience, and a less nostalgic view of what a car should be. Reuters put it plainly last week: Volkswagen has lost ground in China to local rivals that have been quicker to roll out software-rich, lower-cost electric cars. (Reuters)

And the competitive pressure is no longer contained within China. Reuters reported in February that Chinese automakers doubled their share of European car sales to 6% in 2025, even though penetration differs sharply by country. That number is still small enough to dismiss if you want comfort. It is already large enough to demand attention if you care about direction. (Reuters)

So what is actually being revived?

Not Germany’s exact institutions.

Not its exact labour model.

Not its exact premium aesthetic.

What China is reviving is something deeper.

A belief that industrial power matters.

A willingness to align supply chains, policy, infrastructure, technology, and manufacturing around strategic sectors.

A seriousness about export scale.

An acceptance that speed is itself a weapon.

And a refusal to assume that old incumbency deserves permanent reward.

In that sense, China is not simply defeating Germany.

It is reviving, under different political and economic conditions, some of the old industrial virtues that Europe once embodied more confidently than it does today.

That is what makes this moment uncomfortable.

And interesting.

Germany is not finished. But the burden of proof has flipped.

I am not arguing that Germany is over.

That is lazy and ahistorical.

German carmakers still have world-class brands, engineering depth, supplier relationships, global footprints, and serious talent. Volkswagen is adapting. BMW remains formidable. Mercedes still owns parts of the premium narrative. Audi is retooling. Porsche will not disappear because one bad year made the market emotional. (Reuters)

But the burden of proof has changed.

It is no longer enough for Germany to say: we are premium, we are precise, we are engineering-led.

The world is now asking harder questions:

Can you move fast enough?

Can you localise fast enough?

Can you ship software that feels current?

Can you manage energy economics that are no longer friendly?

Can you build EVs that do not merely comply, but excite?

Can you compete when the home market of your rival is also the largest industrial training ground on earth?

Those are not rhetorical questions anymore.

They are operating questions.

What serious operators should watch next?

The first thing to watch is not headline sales.

It is development time.

If China-based design, software, sourcing and vehicle development loops keep compressing while Europe keeps debating, that matters more than one quarter of deliveries.

The second is energy and industrial cost asymmetry.

If Germany remains structurally more expensive to manufacture in, the premium cushion will only stretch so far.

The third is whether Western carmakers become more Chinese in China, and more selective everywhere else. Volkswagen’s Xpeng partnership and “in China, for China” push suggest that the answer is already yes. (Reuters)

The fourth is whether Europe can rebuild industrial confidence without simply copying China.

That is the bigger civilisational question underneath the car story.

Not whether Europe can ban, tariff, or complain its way back into safety.

But whether it can relearn speed, seriousness, and industrial coordination without losing its own strengths in the process.

That is the real contest.

And cars are simply where it is easiest to see.

Why this matters beyond cars

If you work in sourcing, industrial strategy, advanced materials, supplier discovery, manufacturing partnerships, or China-Europe industrial flows, this is not a niche automotive story.

It is a leading indicator.

It tells you where the new industrial clock is being set.

And if you are still reading it as a conventional “German decline versus Chinese rise” story, you are missing the more interesting part.

The more interesting part is that one side is defending an inheritance.

The other is rebuilding a machine.

And machines, when they are well-tuned, are very hard to beat.

- Leon Ge, on behalf of the Tocco team

Private invitation: FutureMade China

A small group of founders, investors, and senior operators will join us in 2026 for a closed-door immersion into China’s industrial frontier - from advanced manufacturing and robotics to AI, biomanufacturing, and the ecosystems shaping the next decade. If you want to see the China that most executives never get access to, apply for an invitation here.