Europe's True Reindustrialisation: First, Look Into the Abyss

If Europe wants the great reindustrialisation, it needs more than speeches.

I say this as someone who owes Europe a great deal. The education I received, scholarships, languages, institutions, and, in all, a seriousness of thought that has been deeply a part of me.

This is exactly the reason why I do not want to sugar-coat the reality for Europe.

If Europe wants a true reindustrialisation, the first thing to do is not another slogan, another conference, another speech on competitiveness. The first thing is to look at where things really stand.

And where things stand is this: significant parts of its industrial system are much weaker than many Europeans still want to admit.

Not that Europe has no excellence left. But excellence is no longer enough when the industrial base is soft, the middle is hollowing out, and too much of the cost structure has turned against you:

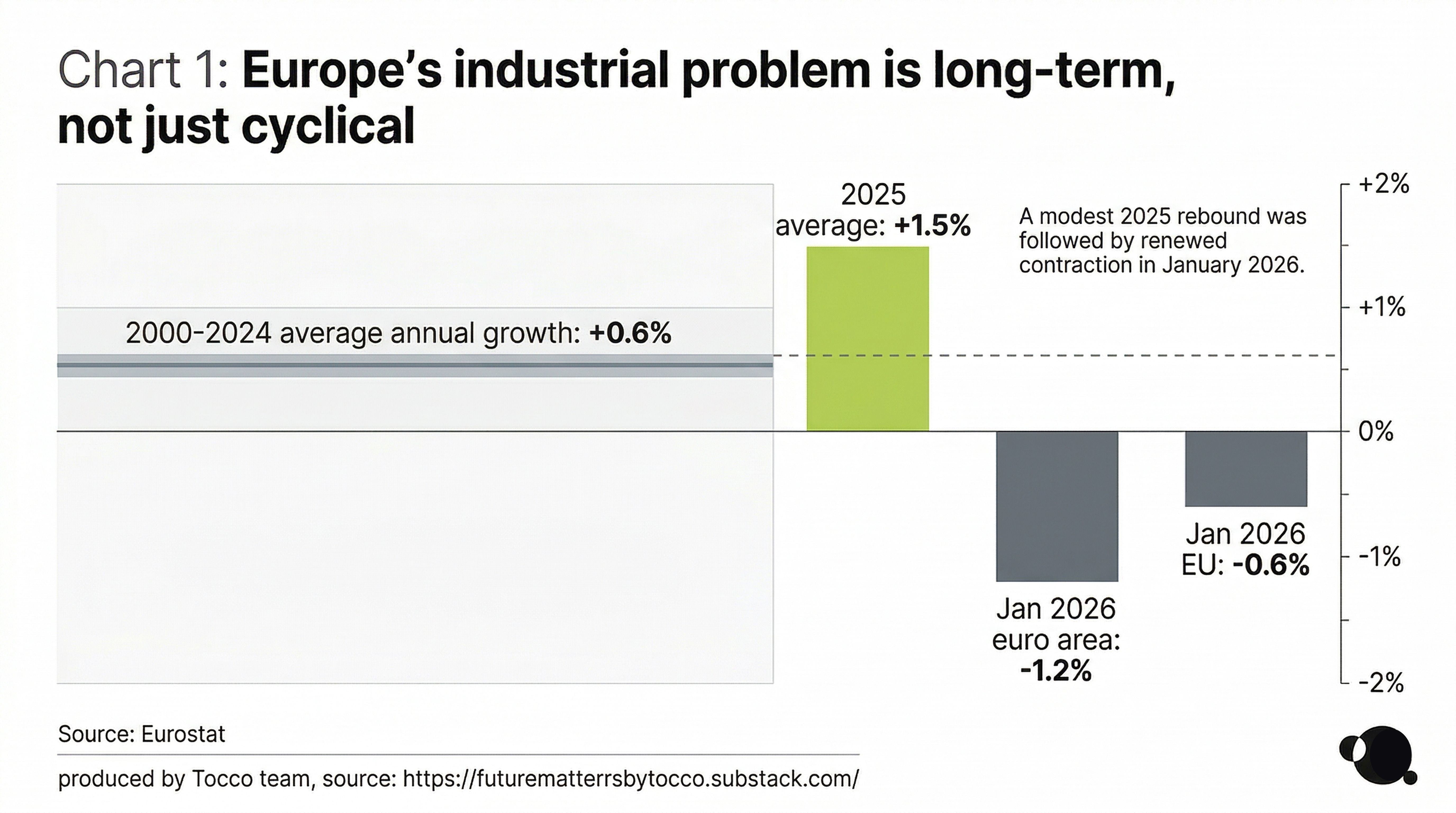

EU industrial production increased by an annual average of just 0.6% between 2000 and 2024.

Yes, 2025 showed a modest average rebound of 1.5%. But by January 2026, industrial production was falling again - down 1.2% year-on-year in the euro area and down 0.6% in the EU.

That is not the profile of a continent in confident industrial ascent. It is more like the profile of a continent fighting against drift.

Across industries: A Crisis of Competitiveness

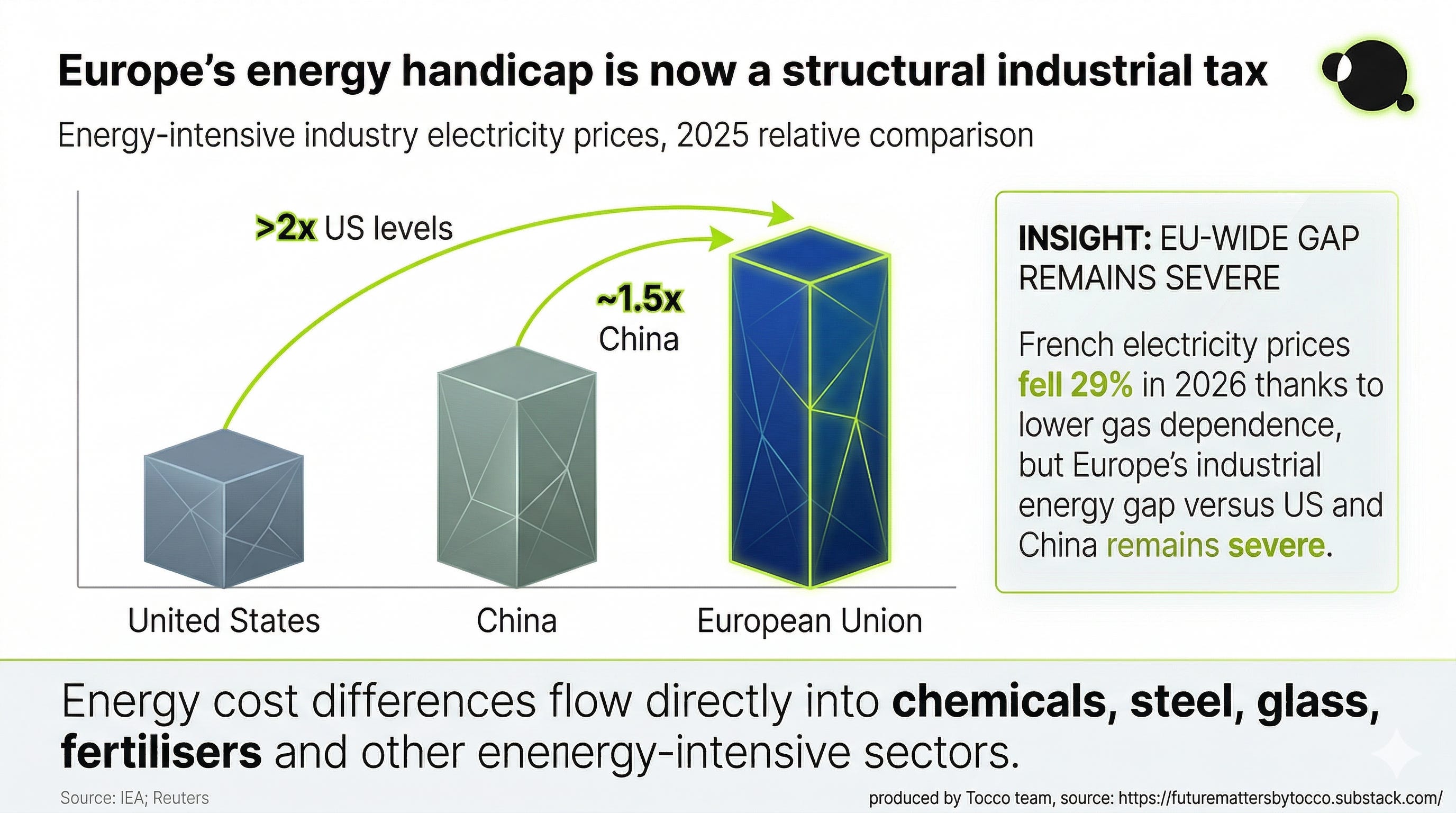

Start with energy, as it is the master variable - sitting upstream of everything else in the physical economy: steel, chemicals, glass, ceramics, refining, fertilisers, paper, aluminium, machine shops, foundries, logistics.

When energy turns volatile, the whole industrial organism starts moving either more slowly, more defensively, or more expensively. The IEA says EU electricity prices for energy-intensive industries in 2025 remained more than twice US levels and nearly 50% above China’s.

In chemicals specifically, Europe’s gas disadvantage versus the US has been brutal. The latest Middle East shock hit this further: Reuters reported that the euro zone economy is close to stalling, with oil up sharply this year, delivery delays worsening, and inflation expectations rising fast.

One of the reasons European decline is so easy to misread is that - like many other cases in history - it often arrives not as one dramatic collapse, but as thousands of executive decisions. Delay this CAPEX. Idle that line. Import this feedstock instead of making it locally. Shift the next plant there, not here. Run the European site for premium or niche output only. This trend doesn’t look temporary.

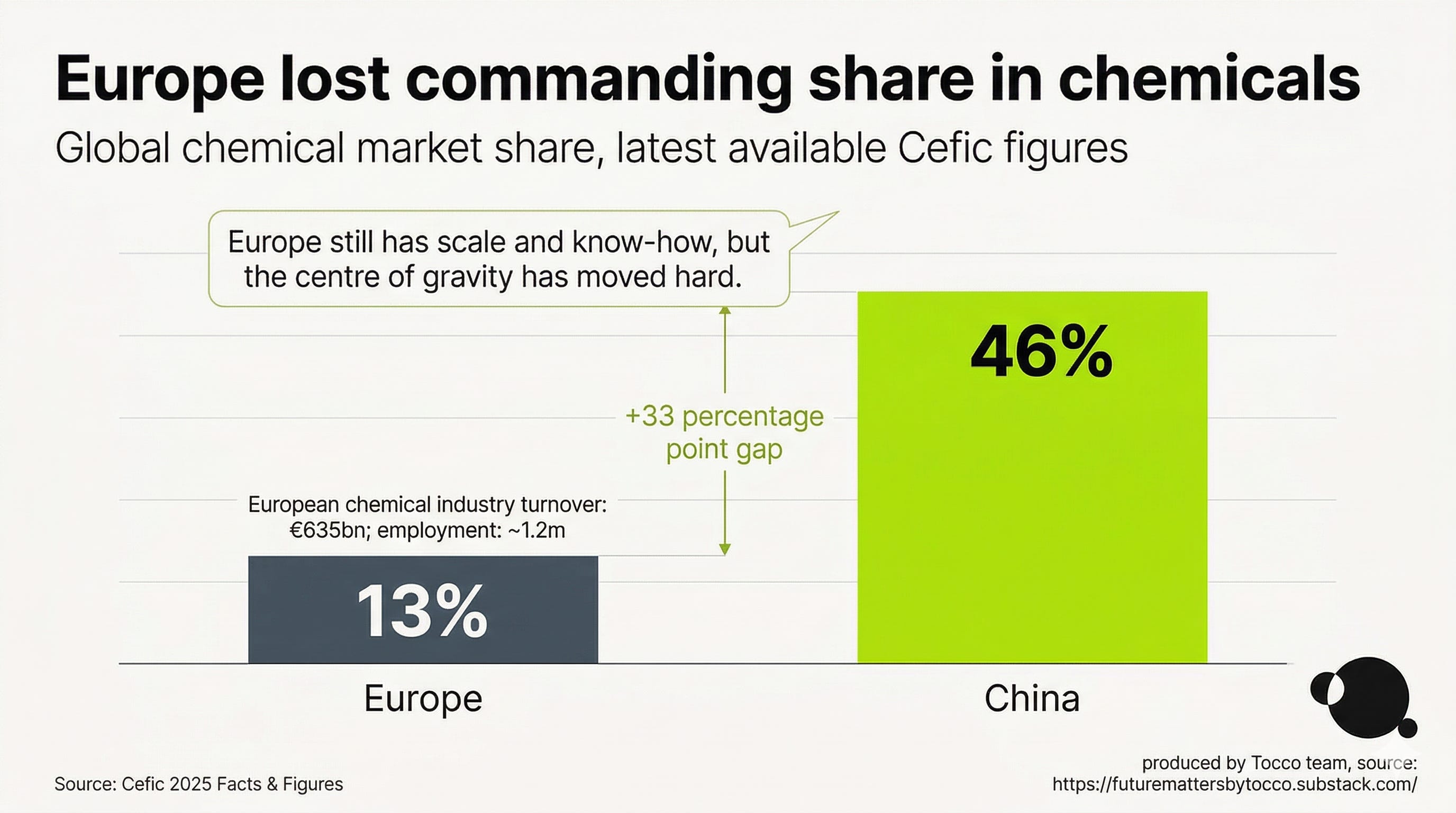

Illustration for this trend found in the chemical industry. Europe’s chemical industry still has €635 billion in turnover, about 1.2 million jobs, deep know-how, and a central position in modern manufacturing. But the centre of gravity has shifted. Cefic says Europe’s share of the global chemical market has fallen to 13%, while China has risen to 46%. BASF, Europe’s flagship chemical company, is at the same time expanding heavily in China while warning investors about weak demand and higher costs at home.

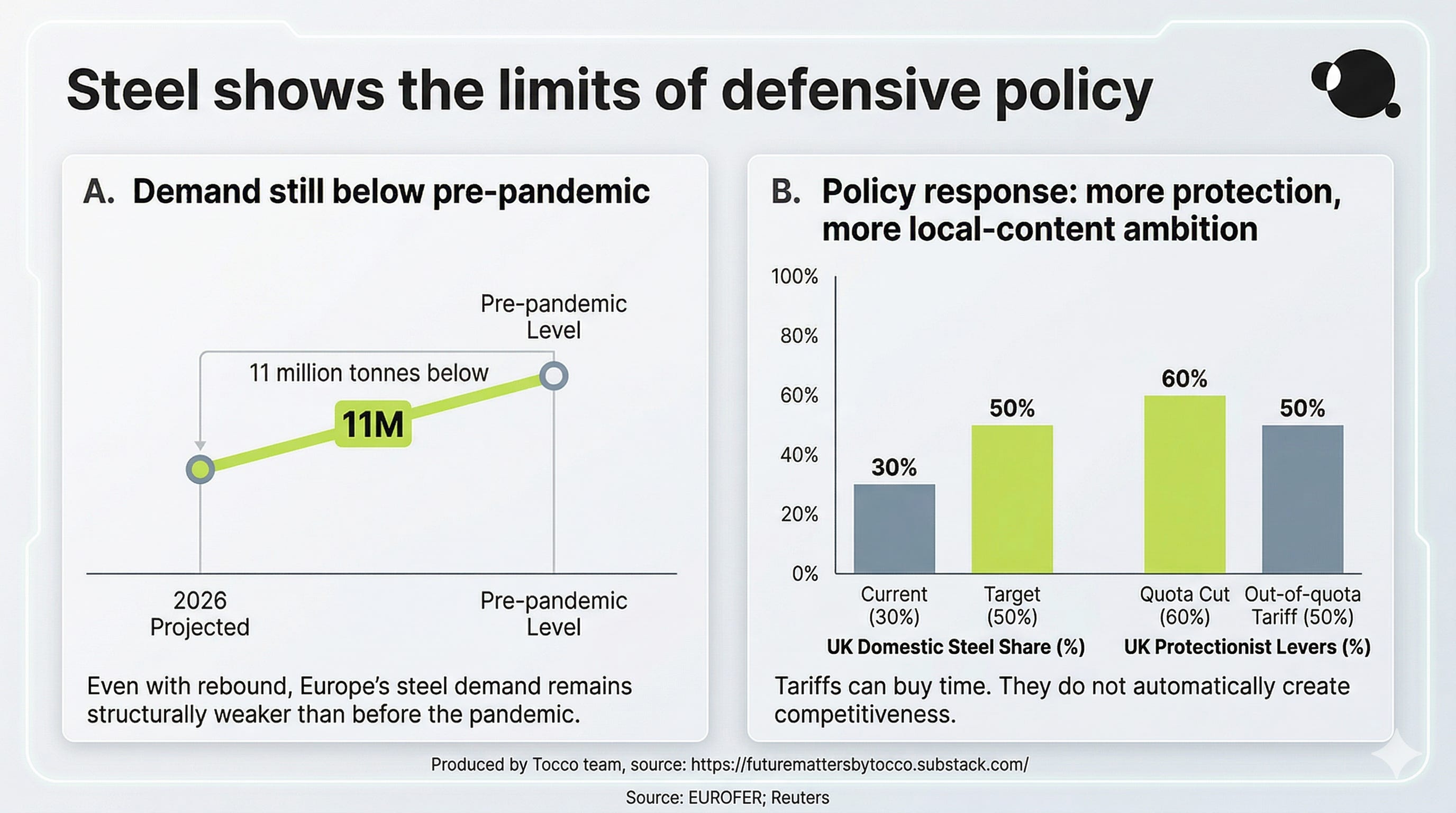

Steel tells a similarly hard truth.

EUROFER reports European steel production hit a historic low in 2025, while imports gained a record share of the EU market. Even if demand rebounds modestly, European steel consumption in 2026 is still expected to remain around 11 million tonnes below pre-pandemic levels. Britain’s response this month: cut tariff-free steel quotas by 60%, raise out-of-quota tariffs to 50%, and explicitly try to rebuild domestic share from 30% to 50%. We can understand the instinct. But tariffs can buy time; they do not, by themselves, create competitiveness.

Automotives follow the same trend.

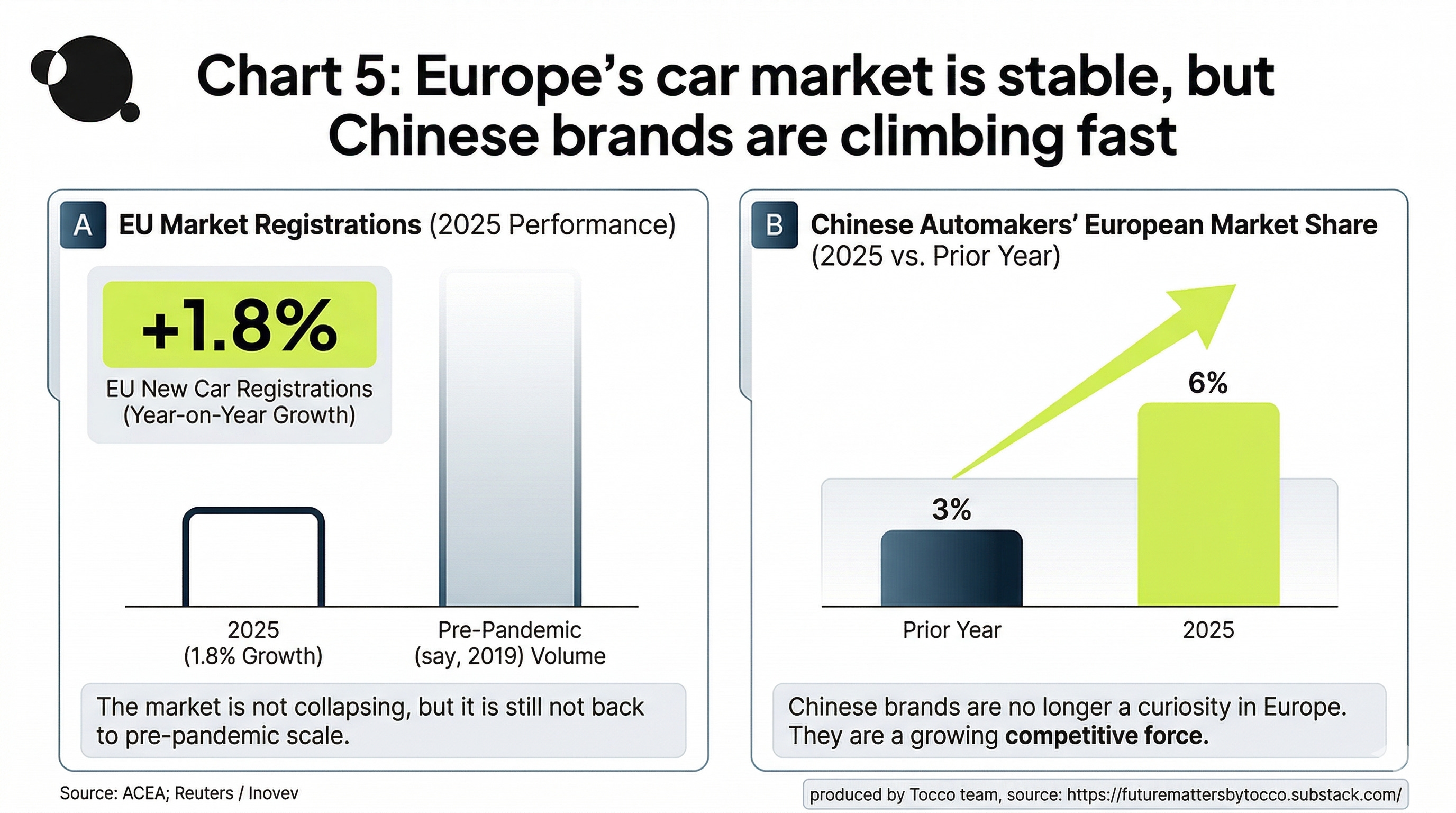

Though Europe still has brand power, engineering prestige, supplier depth, and some of the best industrial storytelling in the world, nothing has been guaranteed. ACEA says EU new car registrations rose 1.8% in 2025, yet volumes remain well below pre-pandemic levels. At the same time, it is reported that Chinese automakers doubled their share of the European market to 6% in 2025.

The battery layer is even more sobering: according to Reuters, the cost gap between EU-made and Chinese batteries is still around 90%, even if scale and better execution could narrow that gap sharply over time. I wrote previously about Germany vs China in the EV race and how it reveals the industrial infrastructures beneath.

Too much European debate still treats China as a geopolitical problem, a subsidy problem, a dumping problem, or a values problem. Sometimes it is all of those things. But that is not the whole story, and serious industrial people know it. China is also a capability problem for Europe, because it has become the toughest real-time industrial proving ground in the world across more and more sectors: EVs, batteries, solar, robotics, manufacturing speed, digital supply chains, and increasingly the fusion of software and hardware.

That is why recent remarks from Mercedes leadership in Beijing matter. At the China Development Forum, Ola Källenius described China as a “dynamic innovation landscape” and stressed Mercedes’ long-term commitment. In Chinese media coverage of the same forum, he was quoted even more bluntly: if you want to play football, you play in the Champions League, and China is the Champions League of the automotive industry. Whether one prefers the diplomatic version or the sharper one, the underlying point is the same: the hardest game is being played there. Serious firms know it.

Resilience vs. Fragmented Policies to treat symptoms

Now, to be fair, Europe is not simply declining across the whole board.

Europe still has aerospace, premium machinery, pharmaceuticals, precision engineering, serious materials science, defence-industrial momentum, and a regulatory machine strong enough to shape markets far beyond its borders. Renewable electricity reached 46.9% of EU net generation in 2024. Battery storage deployment in the EU rose to 27.1 GWh in 2025. Germany’s March flash manufacturing PMI even climbed to 51.7, its highest in 45 months, even as the broader private-sector picture softened.

France is a good illustration of both the resilience and the problem.

Because France, thanks largely to nuclear power, has been more shielded than some gas-heavy peers. Reuters reported that French electricity prices are down 29% this year, while gas-dependent systems such as Italy have been hit much harder. But cheaper power alone has not magically restored industrial momentum. France’s private sector contracted in March at its fastest pace since October, with the flash composite PMI at 48.3 and input-cost pressure rising sharply. So yes, energy architecture matters enormously.

This is the resilience part of the story. But energy relief by itself does not single-handedly rebuild a system that has potentially lost speed, density, and confidence.

Among the problems, the low-end goods parcel flood could be a great illustration.

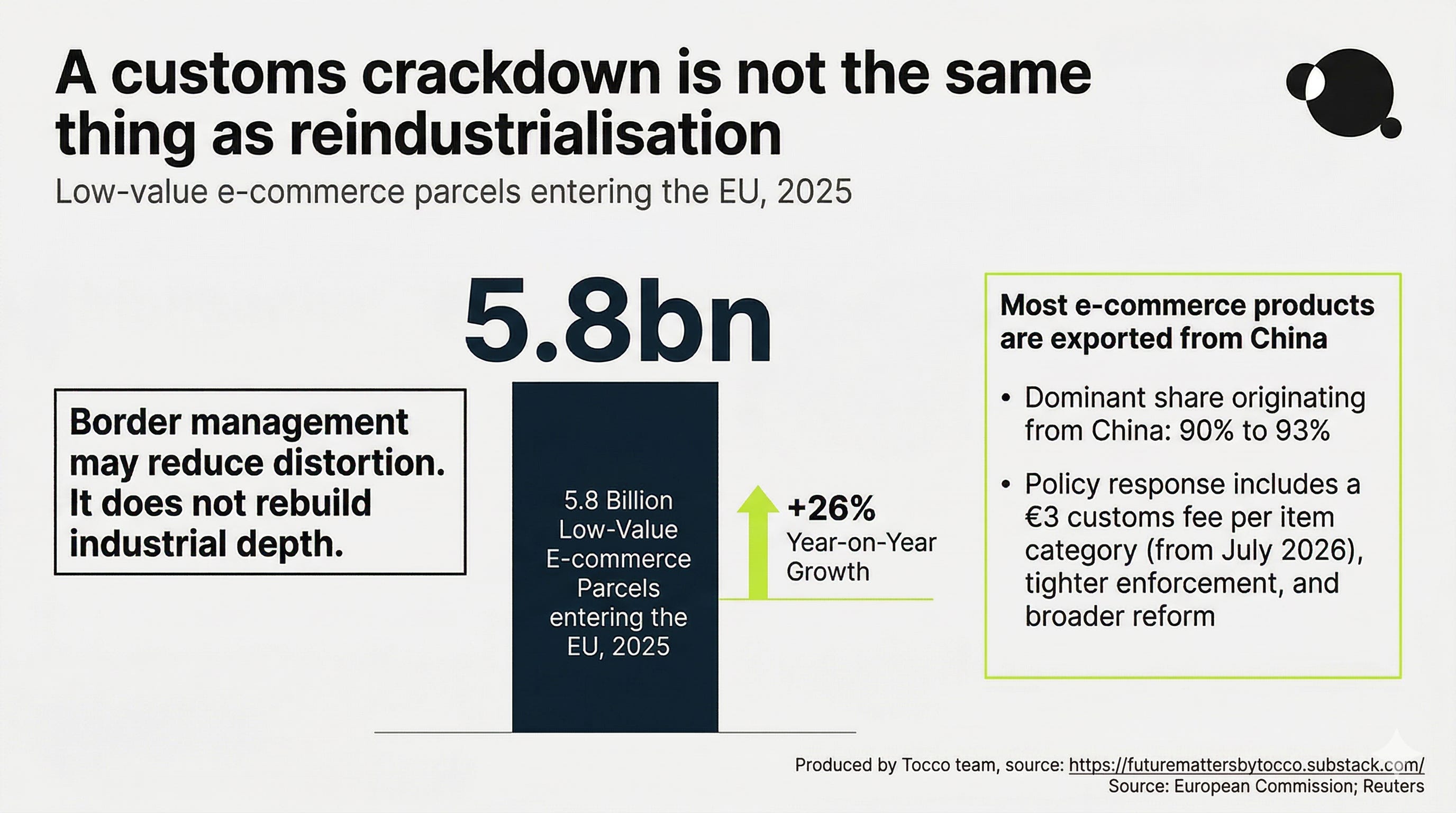

In 2025, 5.8 billion low-value e-commerce parcels entered the EU, up 26% year-on-year, according to the European Commission figures. To shield local French retailers from this competition, the French government imposed a new fee starting March 1, 2026: a €2 flat charge for every individual item under €150 in packages entering France directly from outside the EU.

The policy had a critical flaw: it only applied to packages arriving directly in France. The EU’s core "free movement of goods" rule allows products legally shipped into any EU country to move freely to all other EU member states with no extra fees. Chinese platforms immediately exploited this loophole: they rerouted all their China-origin cargo flights from France to neighboring EU countries (Belgium and the Netherlands). Packages landed there first, then were trucked into France, completely avoiding the €2 fee.

The result was the exact opposite of France’s intent:

No drop in Chinese e-commerce packages to French shoppers - only a change in their delivery route

Severe harm to France’s domestic aviation and logistics sectors: Paris’ Charles de Gaulle Airport saw a 60% plunge in China cargo flights (losing ~50 weekly flights), a 92% drop in e-commerce customs filings, freight industry layoffs, and closure risks for small regional airports

Neighboring EU countries gained all the rerouted cargo and logistics business, becoming accidental winners. This outcome was entirely foreseeable: Italy had implemented an identical policy earlier in 2026, with the same rerouting result.

After all, a customs fee on small parcels is not an industrial strategy. It may reduce distortion, but it does not rebuild tooling, supplier depth, or mid-market manufacturing confidence.

If you gaze long enough into the abyss

This is why I think the honest conclusion is neither declinist nor comforting.

Europe’s problem is not that it has no excellence left.

Europe’s problem is that excellence is becoming too isolated.

Too much of the industrial middle has become fragile. Too much of the energy-intensive base has become uncompetitive. Too many policymakers still confuse prestige with capability.

If Europe wants a true reindustrialisation, it needs more than speeches about sovereignty and more than defensive tariffs at the border. It needs cheaper and more stable industrial energy. Faster permitting. Faster capital formation. Serious local demand support in strategic sectors.

That is the abyss Europe needs to look into.

Not because Europe should give up.

Precisely because it should not.

By Leon Ge

March 24 2026

This essay is the first in a series on Europe’s industrial condition and the harder question of reindustrialisation. I am approaching it as a Chinese operator with deep exposure to the West (10 years in France, 10 years in Singapore) and a strong interest in where industrial capability is truly compounding, where it is fragmenting, and why. The goal is to look squarely at reality and from that, make decisions.

In the next pieces, I’ll go further into where policy, capital, and execution in Europe need to change if reindustrialisation is to mean anything more than a slogan.

Private invitation: FutureMade China

A small group of founders, investors, and senior operators will join us in 2026 for a closed-door immersion into China’s industrial frontier - from advanced manufacturing and robotics to AI, biomanufacturing, and the ecosystems shaping the next decade. If you want to see the China that most executives never get access to, apply for an invitation here.